FinTech Startups Changing the Debt Collection Experience for Businesses & Consumers

Debt collection is not the sexiest segment in the financial services industry. To be honest, the experience just straight-forward sucks for everyone involved in this horrendous process—lenders and borrowers alike. Nonetheless, debt remains a constant in the lives of a massive number of individuals around the world. By the end of Q2 2017, total outstanding consumer debt in the US alone hit $3.7 trillion (+$9.14 trillion of housing debt) – a volume not yet sufficiently addressed neither by financial institutions nor by technology startups, except for a few interesting examples (like True Accord, InDebted, collectAI, Symend, Collectly).

According to the latest International Debt Collections Handbook (USA) published in June 2017, the estimated success rate of collections between 01/2014 and 12/2016 in the United States was just at 36.7% (with the same metric for Canada estimated to be at 17.7%, UK at 65.8%, Mexico at 38.7%, China at 23.9%, India at 17.3%, Germany at 63.9%, and France at 67.8%). Thus, despite the potential market size and almost miserable collections success rate in a large number of developed and developing countries, debt collection startups are some of the most underrepresented ones in the global FinTech community.

Lack of transformative work and attention to this common practice left debt collection practices very retrograded for 2017. It’s almost hard to believe that technology startups addressing this massive issue are the loneliest ones (although, one could argue it’s not a bad thing – the less competition, the better), with a certain regional variance in approach to changing the experience with debt collection. Sofya Pogreb, the former COO of TrueAccord, emphasizes that the barriers to entry into the debt collection business are significant, mentioning that it took TrueAccord over two years to become fully licensed (as most states have separate licensing processes and requirements).

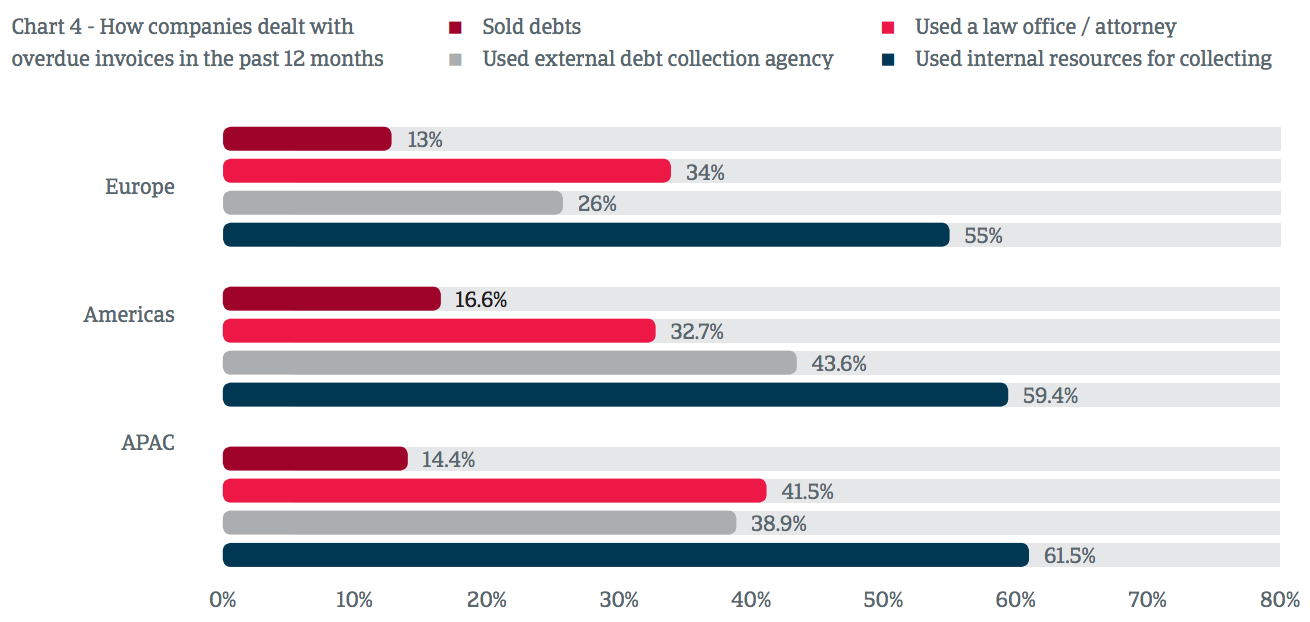

However, the Global Collections Review (Europe, Americas, and Asia-Pacific) by Atradius Collections (a B2B debt collections services company), published in September 2017, reveals that the companies’ attitude towards the collections market is strongly focused on internal management. As a result, the study notes that professional debt collection is still difficult to manage. Still, the approach to alternative solutions offered in the collections market displays a noticeable variance among companies in different countries.

Image source: The Global Collections Review (Europe, Americas, and Asia-Pacific), 2017

Italy, Spain, Germany, France, and Belgium, as well as China, India, Indonesia, Mexico, and Brazil, are found to be more inclined to adopt alternative or additional solutions to traditional debt collection services, compared to the general tendency among the other countries profiled in the report. According to Atradius Collections, companies in Europe appear to be more cautious of using alternative services other than traditional debt collection. Conversely, companies in the Americas and APAC show a stronger openness towards service innovation.

How FinTech is changing debt collection: behavioral analytics, ML, AI, data analytics, and sophisticated communication strategy

So, how exactly are technology startups worldwide intervening to reimagine the debt collection experience? Let’s look at some of them to understand what they bring into play.

InDebted (operates in Australia and New Zealand/UK and the US coming soon), for example, simply moves the whole collection experience for businesses online, offering a portal where clients can monitor the status of collections performed by InDebted representatives. Once InDebted collects the client’s debt and the payment clears, the funds are transferred to the client’s account the same day. The pricing is very clear and transparent, although somewhat hefty, dare I say – the company charges a flat 20% fee on anything it collects.

While the first case roughly reminds of a traditional experience moved online, TrueAccord is probably a bit more interesting case – the company operates a data-driven debt collection platform powered by ML and digital-first communications. TrueAccord’s Patent Pending decision engine uses ML to create personalized, digital-first consumer experiences uniquely tailored for each consumer. The platform uses a machine to create a complex interaction model with a consumer and a clustering engine to compare the consumer to more than 1.5 million consumers who passed through the platform. Then, based on those 100’s of millions of data points, it predicts the consumer’s reaction to communication frequency, timing, channel, and content.

TrueAccord’s decision engine then selects from hundreds of internally generated and legally pre-approved messages that drive consumer engagement via omnichannel delivery. Once delivered, it tracks real-time events from the consumer – email opens, link clicks, browsing patterns on TrueAccord assets, and interaction with the company’s call center – to decide what its next step should be. TrueAccord’s Compliance Firewall enforces compliance rules on contact timing, frequency, and included disclosures. The Compliance Firewall allows implementing new rules at scale, as state-level rules may vary, and keeps a detailed event log for audit purposes.

TrueAccord enables customized offers and payment plans to enable consumers to successfully pay off more of their debt. The platform’s features include behavioral analytics, code-driven compliance, audit trail, real-time personalization, and more. LendUp, Yelp, and UpWork are among the company’s clients.

Another interesting newcomer, Collectly (focuses on medical bills currently), aims to improve creditor collection of the outstanding debt through personalized and automated communication (also, the person who built the platform is an ML expert). The collection service for healthcare providers and medical billing companies combines patient information from multiple EHR systems, analyzes it, and executes collections.

As shared by TechCrunch, while most debt collection agencies still use paper mailings and phone calls in their attempts to recover their clients’ money, Collectly is moving its interactions online (similar to competitors), tracking and collecting data from debtors in how they respond — or don’t respond — to its outreach. By creating a more personalized outreach and collection strategy, the company attempts to provide people who owe money with appropriately structured repayment solutions that allow clients to recoup some of their losses, even if debtors can’t pay the whole amount owed.

We also mentioned a company called collectAI, which provides AI-based collection services to help clients manage account receivables. collectAI’s services include e-invoicing, dunning, and debt collection. The company’s self-learning AI system supports the complete value chain around collectAI’s services, continuously learning and optimizing the result. While the company claims to leverage AI around all services, with debt collection, a strong emphasis is made on efficient, multi-channel communication and UX, rather than applying the technology in a sense as it does in the previous example.

Symend, a Canadian debt recovery solution, claims that US delinquent debt has risen from $150 billion to over $600 billion in the last five years and places current collections tactics into the bucket of ineffective and only yielding a success rate of ~7%. The company claims to combine predictive analytics, automation, and positive collection tactics (a common practice among the technology companies aiming to tackle the issue). The solution combines comprehensive data mining, relationship management tools, and strategic campaign tactics across all customer channels. Predictive analytics drive workflow recommendations, allowing the client’s accounts receivable team to reach more customers through workflow automation. Clients can access complete customer profiles and behavioral tracking while extending payment options and online processing to their customer base.

There are certainly more examples, which vary in how they leverage technology (or not), in offered functionality and business models. But most importantly, they vary in the approach and a heavier focus on one side or another. For example, a class of players offer sophisticated ‘communication scheduling’ software to reduce the collection time but do not particularly emphasize a change in approach from the debtor’s perspective. Others are more advanced in applying the technologies mentioned earlier (cloud, ML, AI, behavioral analytics). Still, again, the emphasis of those companies is on businesses recovering money as effectively as possible, while the debtor’s experience is somewhat on a Stone Age level. A few more examples: Debtor Daddy, InterProse, Simplicity Collection Software, CollBox, Debito, and others.

What are the best markets for a debt collection innovation?

The Insolvency Matrix 2017 provides a relatively comprehensive overview of the tendencies in a particular market, indicating the ones most in need of solutions to improve debt collection.

Image: Insolvency Matrix 2017

The countries with average to highest insolvency rates that are either stable or deteriorating include Denmark, Belgium, Sweden, Switzerland, Norway, and many other developed economies. In the near future, those markets would face the most severe need to change practices and technologies applied to debt collection to turn around the insolvency rates and improve debt management. Overall, global business insolvencies are expected to decrease 3.0% this year and 2.0% in 2018, mainly led by an increasingly robust recovery in the Eurozone.

To learn about Prove’s identity solutions and how to accelerate revenue while mitigating fraud, schedule a demo today.

Keep reading

Prove’s solutions can help businesses make their online customer experiences faster, easier and more secure.

While the rise of deepfake technology is not totally new, its level of sophistication presents new challenges for businesses seeking to deliver frictionless digital onboarding experiences to their customers.

Prove and BetMGM, the sports betting and iGaming leader, have entered into a partnership which will elevate the security standards and user experience for BetMGM customers through the Prove Pre-Fill® identity solution.

Trusted by 1,000+ leading companies to reduce fraud and improve consumer experiences, Prove is the world’s most accurate identity verification and authentication platform.